The software industry is widely seen as one of the industries most exposed to the risks associated with the AI boom. The software-as-a-service, or SaaS, segment is seen as particularly vulnerable, because many of the solutions offered by SaaS firms are at risk of being replaced by AI agents in the not-too-distant future, potentially putting a lot of pressure on what was considered safe, predictable recurring revenue. These fears of AI disruptions have put significant pressure on the valuations of software companies in recent months, leading to concerns for the wider economy.

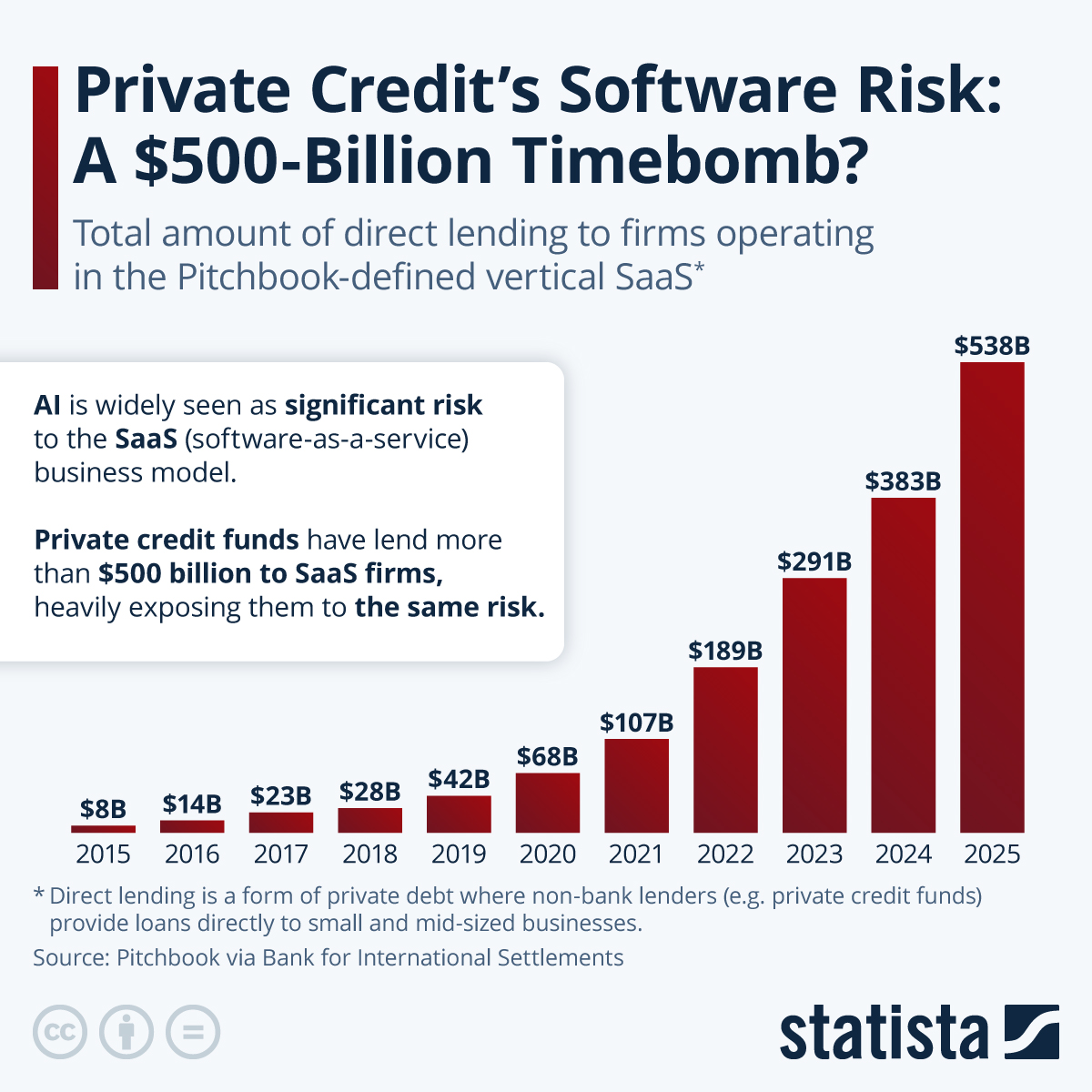

The problem is that the software industry, and especially SaaS, is heavily backed by private credit because its subscription-based revenues are predictable, scalable and thus ideally suited to servicing debt. This makes it attractive for investors seeking stable, income-generating investments, a typical profile for private lenders. As our chart shows, direct, i.e. non-bank, lending to SaaS firms has ballooned from less than $10 billion in 2015 to more than $500 billion in 2025, heavily exposing the private credit sector to the aforementioned AI disruption risks. Some are even likening the situation to the housing bubble, when abundant money and overly optimistic assumptions led to a buildup of high-risk credit, which eventually soured when rising interest rates and slowing home price growth set in motion a vicious cycle of defaults.

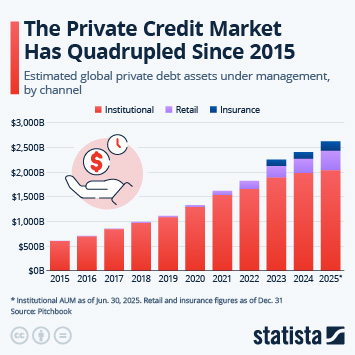

But while there are similarities to the situation that eventually led to the financial crisis, most importantly a lot of money chasing deals, there is one key difference. Unlike the housing bubble, which brought the entire financial system to the brink of collapse, today’s risk isn’t spread through the entire banking system. In this case, the risks are mostly held by institutional investors such as pension funds and insurance companies, so that the fallout from mass defaults could be more contained, while still potentially significant for affected investors.