Almost four years after inflation peaked in 2022, U.S. consumers are still feeling the aftershocks of the inflation crisis, which significantly eroded purchasing power and strained household budgets. Even as inflation moderated, permanently elevated price levels continue to weigh on affordability, helping explain why many Americans are turning to debt not for discretionary spending, but to cover essential costs.

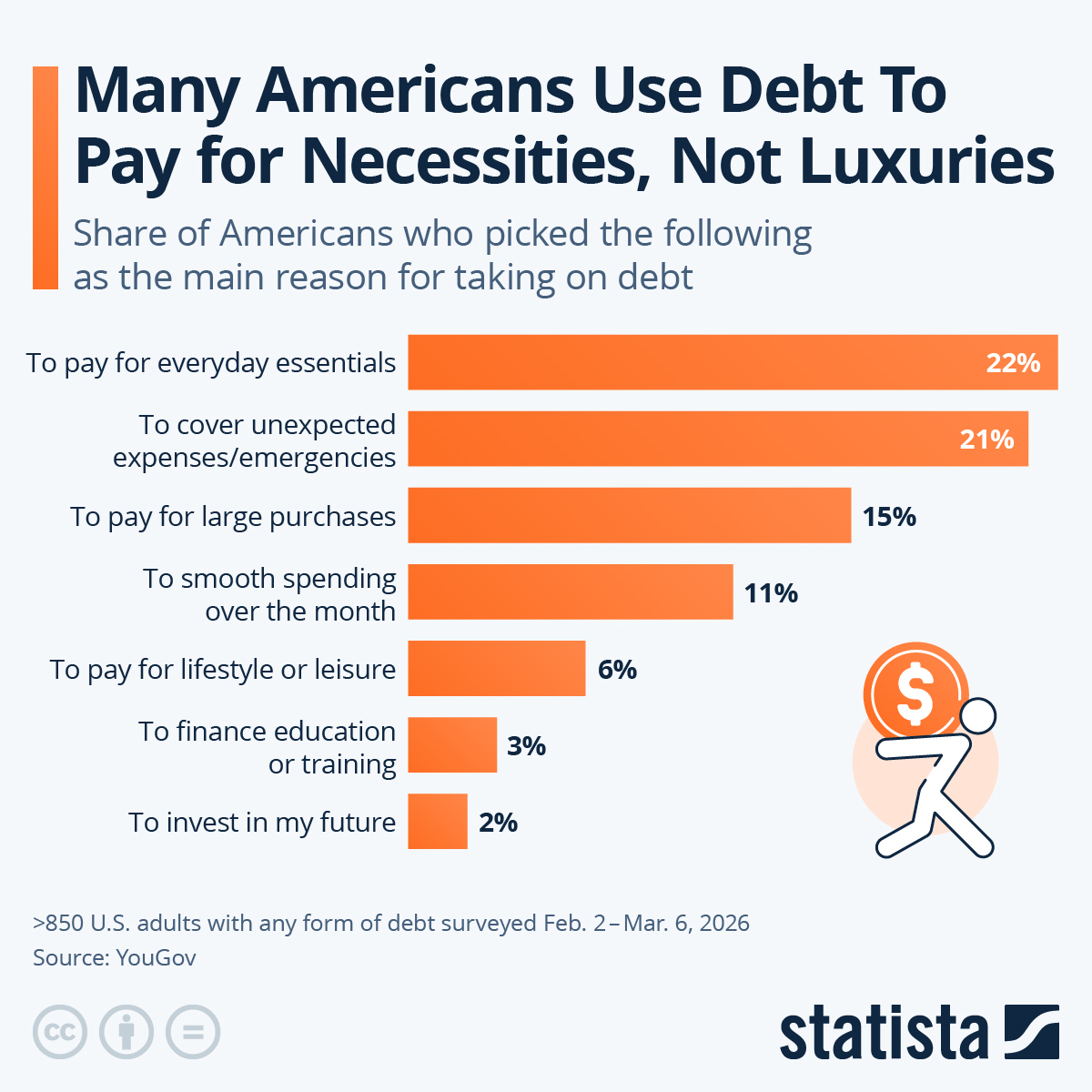

According to a recent YouGov survey, the most commonly cited reasons for taking on debt are paying for everyday necessities and covering unexpected expenses or emergencies, far ahead of lifestyle or leisure spending. Further results from the survey underscore how widespread this reliance on credit has become: 58 percent of Americans report having some form of debt, with credit cards, mortgages and auto loans among the most common forms of borrowing. Notably, 44 percent carry unsecured debt, and more than a quarter of those owe over $10,000, a level that can feel overwhelming to consumers struggling to make ends meet.

In this context, consumer spending trends should be read alongside rising debt burdens and tightening financial conditions. While headline spending may remain resilient, the underlying picture, including greater reliance on credit and less room for savings, is significantly more mixed, raising questions about the sustainability of current consumption levels.