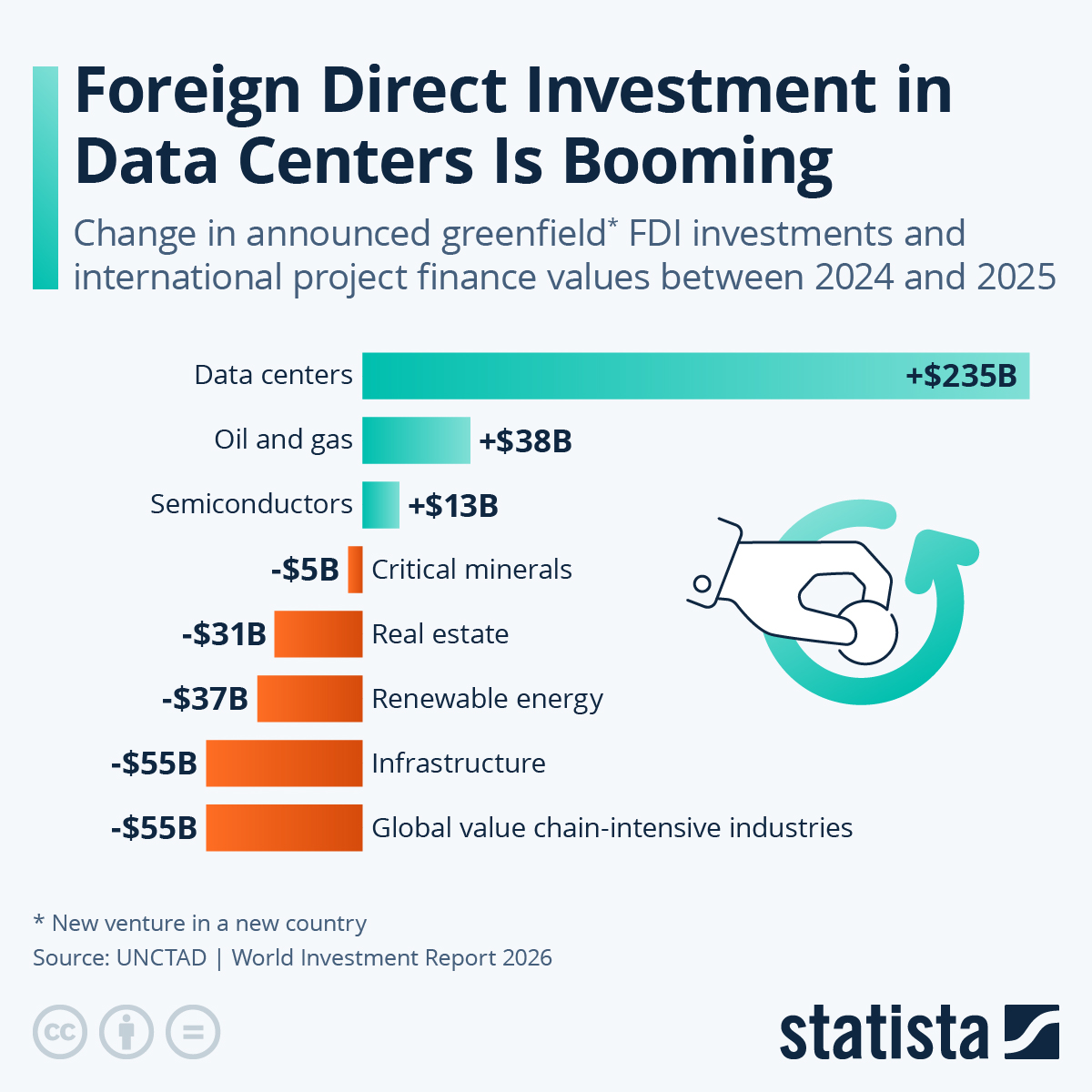

The global surge in foreign direct investments is increasingly focused on digital infrastructure. In 2025, data centers recorded the biggest growth by far among FDI-related investments – an increase of $235 billion in 2025 compared to 2024. They therefore significantly outperformed all other sectors. This is according to the United Nations' World Investment Report 2026.

Other areas are lagging far behind or are even experiencing declines. Oil and gas still saw an increase of $38 billion over 2024, while semiconductors recorded a rise of only $13 billion in this time period. In contrast, there were sharp drops in areas such as infrastructure and global value chain-intensive industries – each down by $55 billion – as well as in renewable energy, which fell by $37 billion. GVC-intensive industries refer to sectors where the production and processing of a product take place across multiple countries. Examples include the automotive industry, electronics and mechanical engineering.

This shift in FDI flows across sectors points to a strategic realignment: Investments are flowing into the digital foundation of the economy, such as cloud computing, AI and data processing, to a higher degree. The decline in some traditional and even some future-focused sectors like renewables and critical minerals indicates that capital is being focused more heavily on growth and technology-driven areas in the short term or that investments are kept at home. This has increasingly been the case with sectors identified as important to national security, like semiconductors or critical minerals.