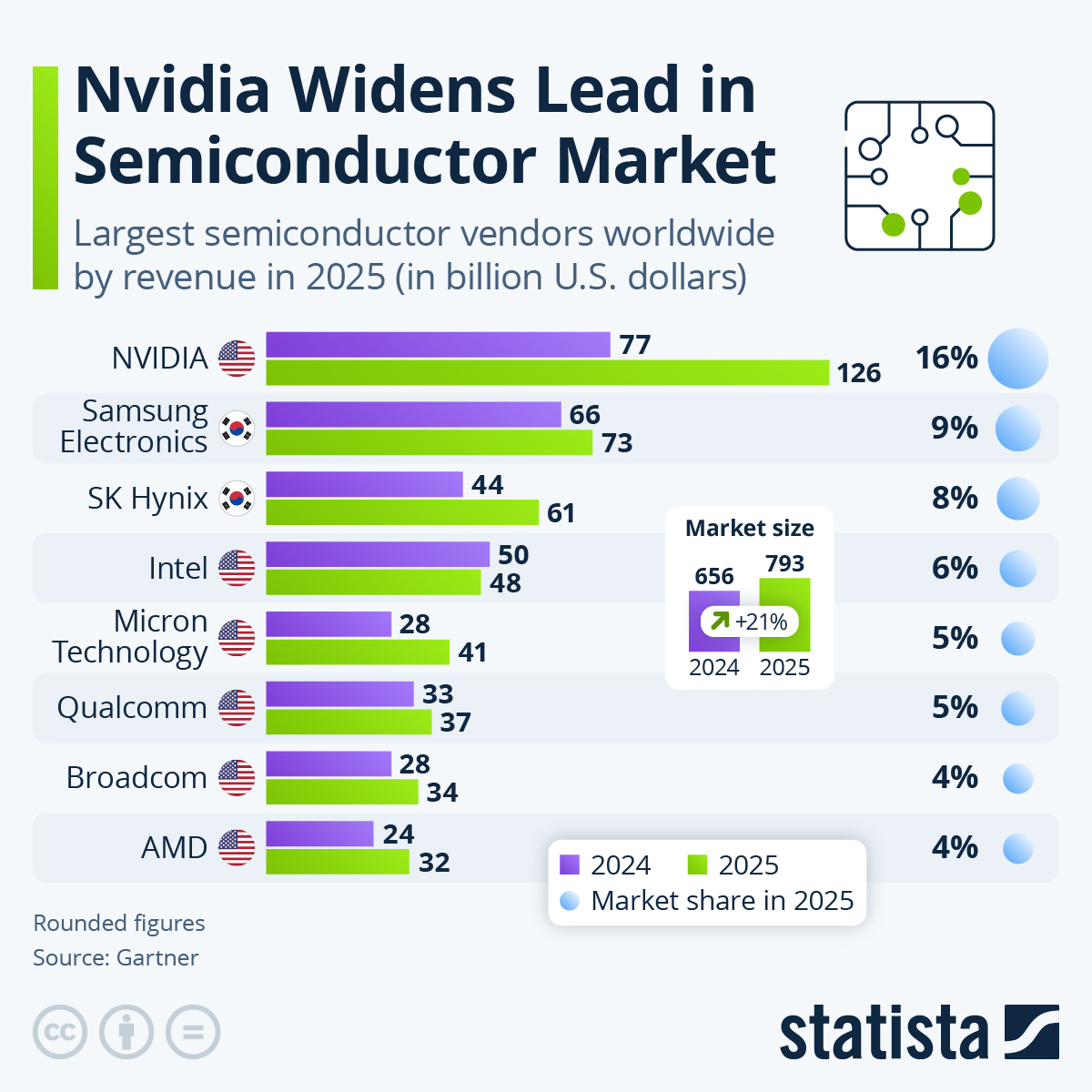

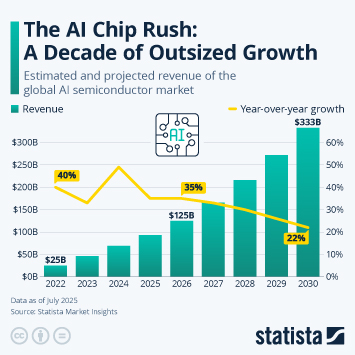

The global semiconductor industry is broadly split between companies that design and sell chips and those that manufacture them, known as semiconductor foundries. While firms such as TSMC dominate chip production, our chart focuses on the largest semiconductor vendors by revenue. Such companies develop and market chips for applications ranging from data centers to smartphones. According to Gartner, worldwide semiconductor revenue rose by 21 percent to $793 billion in 2025, underscoring strong demand across the sector, particularly for AI-related hardware.

As our chart shows, Nvidia’s revenue jumped to $126 billion in 2025, up sharply from $77 billion a year earlier, giving the company a market share of around 16 percent and putting it well ahead of Samsung Electronics and SK Hynix. The surge reflects exceptional year-on-year growth of roughly 64 percent for Nvidia, alongside strong gains among other AI-linked players, including Micron (+50 percent), SK Hynix (+37 percent) and AMD (+35 percent). By contrast, Intel was one of the few top vendors to post a slight decline, highlighting how unevenly the AI boom is benefiting different segments of the industry. This imbalance is particularly evident in Nvidia’s dominant position in the AI accelerators segment (e.g., data centers), where it is estimated to command between 70 and 80 percent of the market.

Recent results suggest that Nvidia’s momentum is continuing into 2026. In the first quarter of its fiscal 2027 (ended April 26, 2026), the company reported revenue of $81.6 billion, representing an 85 percent year-on-year increase, driven primarily by its data center business, which accounts for the vast majority of its sales.