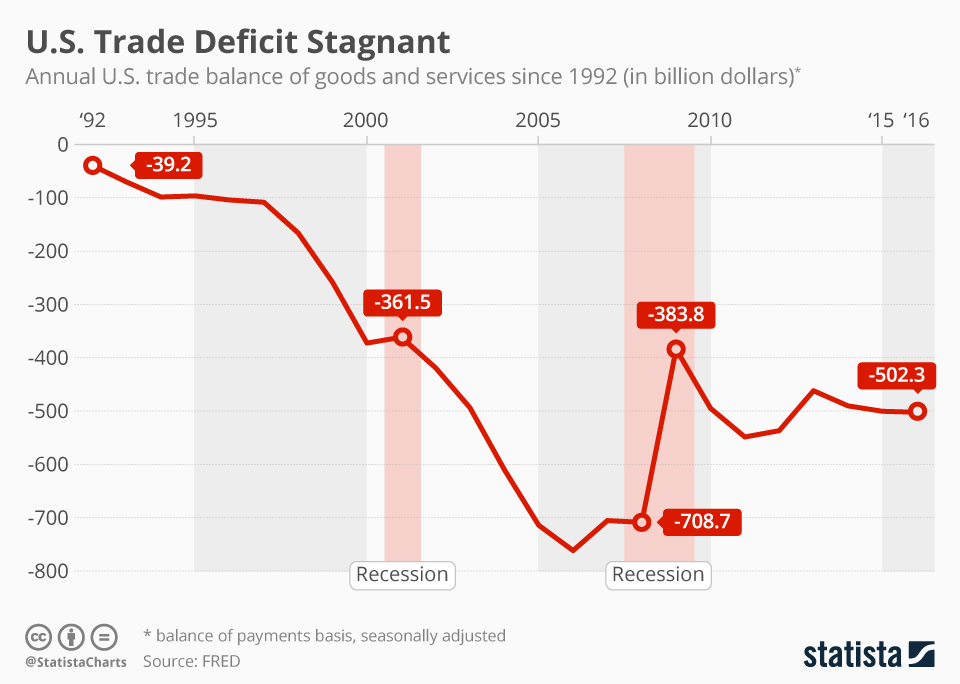

One year after “Liberation Day” tariffs were reintroduced under Donald Trump, the debate over their effectiveness in reshaping U.S. trade remains ongoing. What impact have they actually had on the country’s trade balance? According to data published by the U.S. Bureau of Economic Analysis last month, the American trade deficit remained stubbornly high in 2025, hovering near record levels despite the protectionist measures of the Trump administration.

After narrowing sharply in the wake of the global financial crisis (from -$712 billion in 2008 to -$395 billion in 2009), the deficit widened again throughout the 2010s, reflecting a steady recovery in domestic demand. It increased further during the late 2010s, even as tariffs on Chinese goods were introduced, a trend many economists attribute to strong consumer spending and a relatively strong U.S. dollar, which makes imports cheaper and exports less competitive.

The deficit surged to unprecedented levels during the Covid-19 pandemic, peaking at -$924 billion in 2022, as U.S. demand for imported goods spiked while global supply chains remained disrupted. Although it narrowed somewhat in 2023, it has since widened again, reaching around -$904 billion in 2024 and -$912 billion in 2025.

According to institutions such as the Bureau of Economic Analysis and the IMF, trade balances are primarily driven by macroeconomic factors, such as savings and investment imbalances, rather than tariffs alone. In that sense, recent trade policies appear to have had a limited impact on the overall deficit, which continues to reflect strong domestic demand and structural factors in the U.S. economy.