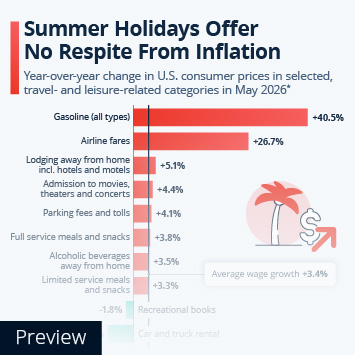

It's been four years since inflation peaked at 9 percent in June 2022, and yet many Americans are still reeling from the lasting effects of the inflation crisis. Despite wage growth outpacing inflation for 34 consecutive months between May 2023 and March 2026, real wages still haven't returned to 2021 levels, leaving many Americans with less buying power than five years ago. And just when real wages had almost caught up, the war in Iran began, sending energy prices soaring and causing inflation to surge from 2.4 percent in February to 4.2 percent in May. At the same time, nominal wages grew only 3.4 percent, meaning that real wages are once again declining.

Between April 2021 and April 2023, inflation had outpaced nominal wage growth for 25 consecutive months, leaving a hole in the pockets of millions of Americans. Despite making more money on paper - nominal wages continued to grow throughout the inflation crisis - consumers were able to afford less than they were before, a situation that is as frustrating as it is economically unsustainable. As anyone who has ever taken a pay cut knows, there are few things more discouraging than putting in the same amount of work in for less money, which is why it’s understandable that inflation has been at the very top of many Americans’ list of concerns for the past years. From an economic perspective, it's also crucial for real wages to increase over time, as consumer spending is by far the biggest component of the gross domestic product and a key driver of GDP growth. In recent years, consumer spending has been surprisingly robust in light of the circumstances, but many Americans were forced to deplete their savings or take on new credit to keep spending.