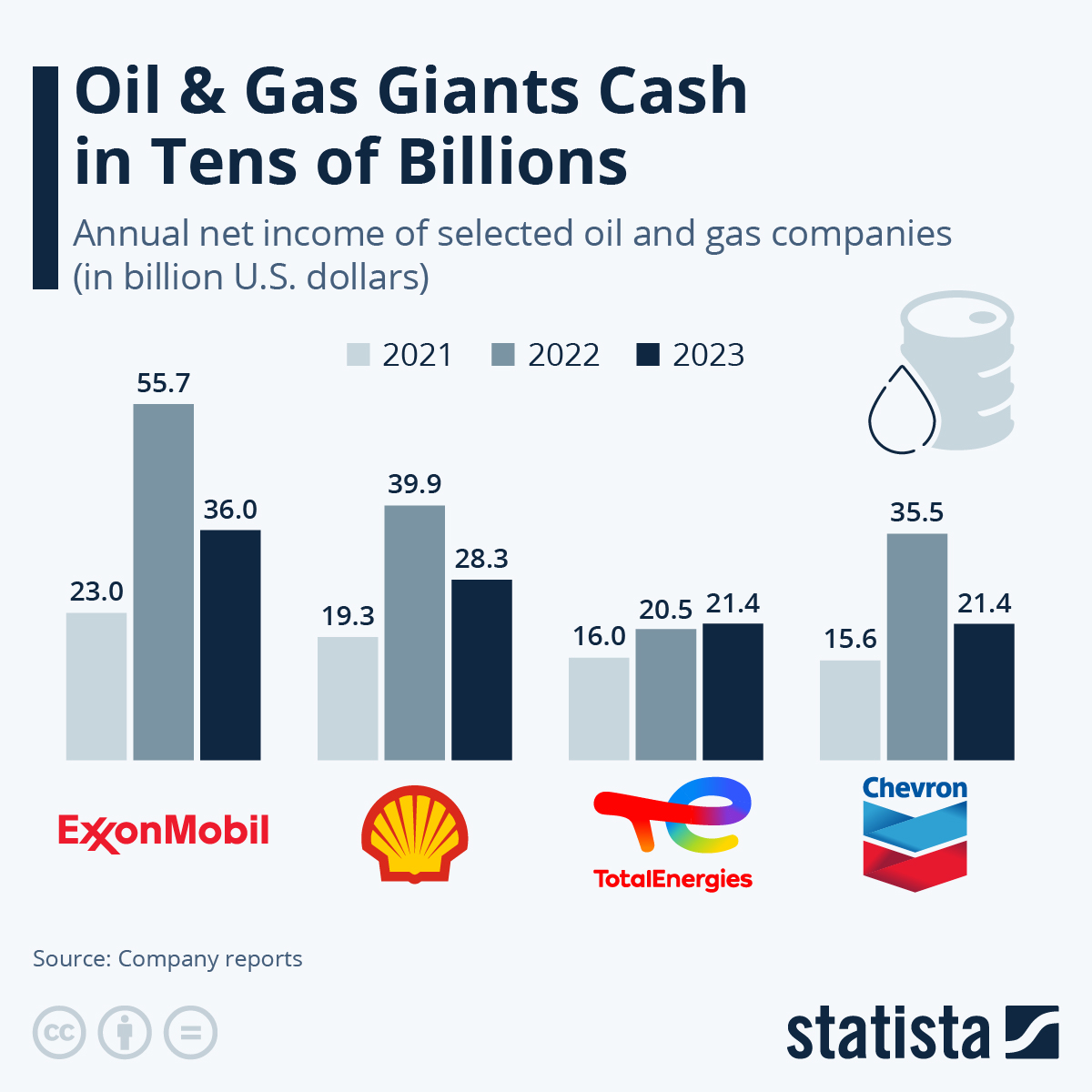

The 2026 Strait of Hormuz crisis has had a mixed impact on the world’s largest oil companies' earnings, highlighting diverging business models rather than delivering a uniform boost to profits. As our chart shows, first-quarter earnings in 2026 moved in different directions among the five Western oil majors, with profits rising at European firms while declining at their U.S. counterparts.

Shell and TotalEnergies both reported solid growth compared to Q1 2025, with earnings up by around 24 percent and 29 percent, respectively, while BP posted a sharp rebound of roughly 132 percent after a relatively weak prior year. By contrast, U.S. giants ExxonMobil and Chevron saw a steep drop in earnings, falling by about 46 percent and 37 percent year-on-year. However, despite this recent partial rebound, earnings across the sector remain below the elevated levels seen in 2024 following the 2022–2023 energy crisis, partly because the latest price spike only affected the final weeks of the quarter.

According to industry experts, the divergence seen in Q1 2026 reflects structural differences in how these companies generate income. U.S. majors, with greater exposure to upstream price realization and domestic shale production, have faced margin pressure despite higher oil prices. European firms, on the other hand, have benefited more from trading operations and LNG portfolios, which tend to profit from market dislocations and volatility triggered by geopolitical shocks.